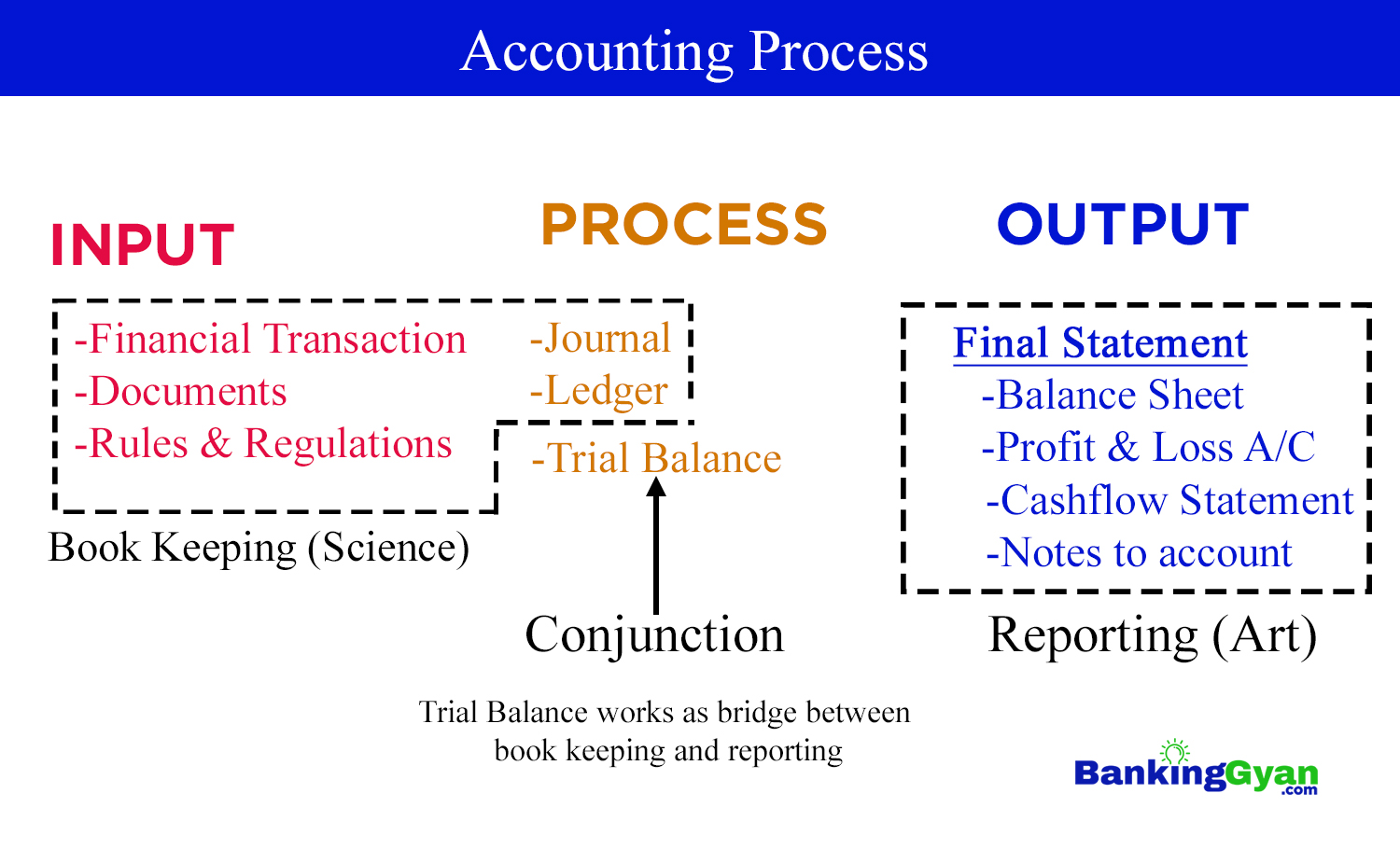

Accounting is the process of identifying financial transactions, systematic and scientific record keeping, classifying, summarizing, and preparing a final statement to provide information to the concerned stakeholders.

- Accounting is the language of business and a mirror of financial transactions.

- It is the art and science of record-keeping and bookkeeping for reporting.

- It is the combination of records, reports, ledgers, and financial documents that are related to legal transactions.

- We can draw a definition of accounting from the input, process, and output concept as shown in the following diagram.

Accounting Principles – Generally Accepted Accounting Principles (GAAP)

Those concepts that are accepted by the universal mass are called principles. The accounting concepts that are universally accepted are known as accounting principles. These principles are also called Generally Accepted Accounting Principles (GAAP). There are basically 10 accounting principles. They are

- Money measurement concept

- Business entity concept

- Single entity concept

- Cost/cash basis concept

- Accrual basis concept

- Double-entry concept

- Going concern concept

- Matching concept

- Historical cost concept

- Accounting period concept

Money Measurement Concept

The money measurement concept defines that only monetary transactions that can be expressed in monetary value are recorded in accounting. Non-monetary transactions are not recorded in the accounting system.

Business Entity Concept

It is also known as the Economic Entity Assumption; the concept holds that the business and the owner are separate entities and must be treated separately. Even for sole proprietorship firms, financial activities must be kept strictly independent from the owner’s personal finances.

Single Entity concept

If there are no debit and credit rules in accounting activities and only personal accounting, including cash and cash content of real accounts are recorded, then this type of accounting approach is known as the single entity concept. This concept is only used in the household sector, but not in the business and organizational sector.

Cost Basis/Cash Basis Concept

Accounting keeps a record only of cash-based transactions of a given period of time. This concept excludes receivable and payable transactions.

Accrual Basis Concept

The accrual basis concept tells that the business transaction includes cash, receivables, and payable transactions. All the transactions that happen over a given period of time should be included in the accounting. It records the revenue when earned and records the expenses when incurred, regardless of when cash is exchanged.

Double Entry Concept

If every financial activity is recorded by using the rule of debit and credit, then such a modern, fundamental, systematic, and scientific concept of accounting is called the double-entry system.

Going Concern Concept

While performing accounting activities, it should be considered that the organization will run forever. This concept defines the rule of accounting preparation with the mindset that the organization never terminates. i.e., organization runs on a perpetual succession basis, meaning the organization continues to exist and operate independently of its members, directors, or owners.

Matching Concept

There must be coordination between the income and expenses of the entity. Those expenses that are related to income-generating activities within a given period of time should be recorded. (Concept of if you invest, you should get a return).

Historical Cost Concept

The historical cost concept tells that organizations record financial transactions considering the original price, not the market price. The valuation of the fixed assets should be recorded in their original price, not in their current value.

Accounting Period Concept

Every 12 months should be considered as an accounting period or fiscal year for the recordkeeping and reporting of financial transactions. The accounting period concept is also called the periodicity concept.

Relates Post