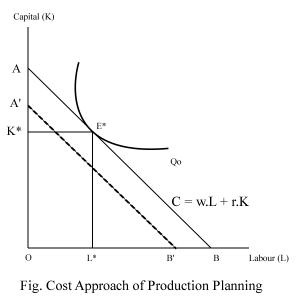

1) Cost Approach of Production Planning:

This approach of production planning aims to minimize the cost. If the output is given ot pre-determined, then the objective of the firm is to minimize the cost and make the production planning accordingly.

In order to explain this, consider there are two inputs, capital (K) and labour (L), and the output is given as. Qo.

i.e. Objective: Minimize Cost (Min. C = wL + rK)

Subject to Qo = f(L,K)

Where W is the wage rate, and r is the interest rate.

In this case, the firm is planning to minimize the cost by using K and L for the given output Qo.

Let us assume that the production function can be represented by the usual shape of the ISO-quants, which are downward sloping and convex to the origin. Then, the cost for the given level of output is said to be minimum if the following two conditions are satisfied.

First order condition (FoC)

Slope of iso-quant = slope of iso-cost

Second order condition (SoC)

Isoquant must be convex to the origin at the point of tangency with iso-cost.

A’B’ and AB are the different isoquants representing a lower cost than AB. So, for the cost-minimizing firm, A’B’ is preferable, but the given level of output Qo is not possible from A’B’.

In the figure, both conditions of cost minimization for the given level of output are satisfied at E*. So, the firm minimizes cost for Qo level of output by employing OL* and OK* units of labor and capital respectively.

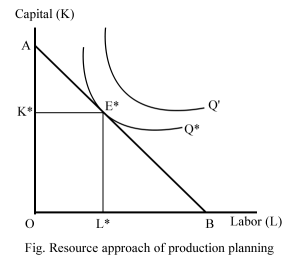

2) Resource Approach of Production Planning:

Under this resource approach of production planning, the firm tries to maximize the output from the given resources. It means the firm has the resources, such as land, labour, and capital, etc., which are given or fixed in quantity.

Since the objective of the firm is to maximize profit, the firm tries to maximize output from the given resource.

To explain this, Ro is the given financial resource, K and L are the capital and labor with respective prices (r and w). The production function is given as Q =f(K, L)

Now, the objective of the firm: Max. Q = f(K, L)

Subject to: Ro = r.K + w. L

As the resource is given, the firm’s planning is to use this resource between capital and labor (K & L) in such a way that it gives the maximum output. To explain this, we assume that the output can be represented by the usual shape of the isoquant, which is downward sloping and convex to the origin. Then the output from the given resource is said to be maximum if the following two conditions are satisfied.

First order condition

Slope of Isoquant = Slope of Isocost

Second-order condition

The isoquant must be convex to the origin at the point of tangency with the isocost.

- Here, AB is the given isocost, which represents the given resources Ro.

- Q* and A’ are the isoquants representing different levels of output where Q’>Q*.

- Since the objective is to maximize output from the given resource, Q’ is preferable but not attainable from the given resource.

- Q* is the attainable/possible from the given resource.

- So, the firm produces Q* level of output as both conditions of output maximization are fulfilled at E* for the maximum possible output Q*, the firm employs OL* & OK* units of labor and capital, respectively.

Q) How is the resource approach of production planning carried out?

Ans-

- 1) Identify the given resource (R1)

- Identify the production function (Q) Q = f(C,L)

- Define the objective Max Q = f(K,L)

- Determine the maximum possible output from the resource.

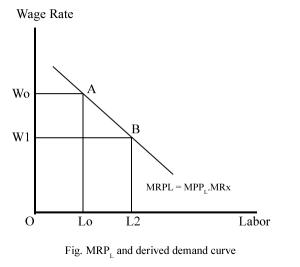

Marginal Revenue Product (MRP) and Derived Demand:

It is the additional revenue to the firm due to an additional unit of labor employed.

- MRPL > W = L ↑ (W = Wage Rate)

- MRPL < W = L ↓

- MRPL = W = L ‘

The demand for any factor or input is the derived demand, which depends on the demand for the goods and services produced by the input.

So, the demand for the input depends on the marginal revenue product of the input, which is defined as the additional revenue to the firm due to an additional unit of the factor/input employed.

To explain this, consider labor as an input where the wage rate is (W), and labor is used to produce the ‘X’commodity. Then the demand for labor depends on the demand for ‘X’, where if the market demand for X is increasing, then the demand for labor also increases. Since the firm is rational and tries to maximize profit, it compares the wage rate and the marginal revenue product of labor (MRPL ) in order to decide on labor demand.

Here, wage rate (W) is labor cost, and MRPL is revenue from the extra labor. So, id MRPL >W (per unit). Then the firm demands more labor.

If MRPL <W, then the firm reduces labor employment demand.

So, the firm is in equilibrium when MRPL = W.

Here, if the wage rate is Wo, then the firm attains equilibrium at “A” where MRPL = Wo by employing OLo units of labor. If the wage rate declines from Wo to W1, then the firm is in equilibrium at “B” by employing LO2 units of labor.

This shows that if the wage rate declines, the firm demands more labor, which means there is an inverse relationship between the wage rate and the quantity of labor demanded by the firm.

This inverse relationship between wage rate and labor is represented by the MRPL curve, and so, the MRPL curve itself is the demand curve of labor by the firm.

Therefore, the demand for an input is derived demand, and the MRP curve of the input itself represents such a demand curve.

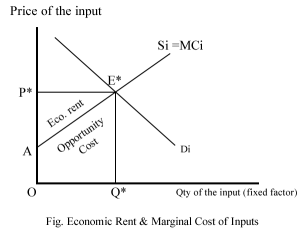

Marginal Cost of Inputs and Economic Rent, Productivity

Economic rent is defined as the payment made to an input (factor) in excess of its opportunity cost. It means economic rent is the difference between the total earnings of the input and the opportunity costs.

i.e., Economic Rent = Total payment made to the inputs – Opportunity cost of the inputs.

The opportunity cost of the inputs is calculated in terms of their marginal cost (MC), where the MC represents the supply of the input itself. The price of the input is determined by the interaction between its demand and supply.

Here,

- Di is the market demand of the fixed input, and Si is the market supply.

- Si itself represents the marginal cost of the input (MCi)

- The input market is in equilibrium at E*, where OQ* is the equilibrium quantity, and P* is the price of the input.

Now,

- Total earning of the input = 🔲OQ*E*P*

- Opportunity cost of input = 🔲OQ*E*A

- Economic Rent = ΔP*E*A

So, the economic rent is the excess earnings of the fixed input over its marginal cost. This shows that the economic rent is also the producer’s surplus. Economic rent is the reward for the efficiency of the input. More efficient input receives more economic rent.

Other posts