Chapter – Decision Analysis

Decision under certainty and uncertainty:

Certainty in decision analysis refers to the situation in which the decision maker has complete and reliable information on all possible alternatives and outcomes, and on the cause-and-effect relationships among the activities and outcomes.

In such a situation, the outcomes are known with 100% accuracy, and the data are complete and accurate. So, the decision maker can select the best alternative to meet the objective, and there is no chance of making a decision error.

The situation of certainty arises when decisions are routine, structured, or programmed. For example, the production decision when demanded is guaranteed or pre-ordered in a situation of certainty.

In this situation, the firm can produce those units that are pre-ordered or guaranteed.

Uncertainty in Decision Analysis

In the situation of uncertainty, the probability of the occurrence of the possible outcome is unknown. So, the decision maker cannot identify the outcomes exactly. There are different alternatives, but their possible outcomes can not be pre-determined with exact probability.

So, there is a chance of making a decision error.

The situation of uncertainty occurs if the information is incomplete and unreliable. There is a changing behavior of the consumer and supplier, the technology is changing more rapidly, and there are unexpected economic shocks and natural disasters.

In such a situation, the decision maker does not have exact information on the outcome of the events/activities.

Despite the situation of uncertainty, the decision maker has to make a decision using some decision rules to optimize the objectives by minimizing the decision error. For example, if the firm is launching a new product in the market without any knowledge of the market preference, this is a situation of uncertainty because the success or failure of the product can not exactly be pre-determined.

Decision-Making Criteria Under Uncertainty

There are different criteria used to decide in the situation of uncertainty, they are:

- Pay off Matrix Analysis

- Decision Tree Analysis

- Expected Utility Analysis

Pay off Matrix Analysis

A payoff matrix is the matrix of the possible outcomes from the different alternatives under the various states of nature, which are outside the control of the decision maker.

Based on the payoff matrix, the decision maker selects the best alternatives depending on the behavior of the decision maker.

To explain this, assume that a decision maker considers three different alternatives for investment, such as a bond, equity, and a mutual fund, and the state of the market or the economy may grow, remain stable, or decline.

Which the decision maker can not control.

Consider the following payoff matrix for this

Scheduling table

| Alternatives | Grow | Stable | Decline | Max | Min |

| Bond | 15% | 10% | 5% | 15% | 5% |

| Equity | 25% | 20% | -15% | 25% | -15% |

| Mutual Fund | 20% | 15% | -10% | 20% | -10% |

This is the payoff matrix, which shows the possible returns from Bond, Equity, and a Mutual fund. Under the different states of the economy.

Based on this payoff matrix, the decision maker or manager selects the best alternatives for the investment, and it depends on the expectation about the market.

A) MaxiMax Criteria (Risk Lover): If the decision maker is optimistic or a risk taker, s/he uses MaxiMax criteria. Under this criterion, the decision maker selects that alternative which gives the maximum out of the maximum.

In this example, 25% is the maximum out of maximum return given by the equity. So, the optimistic investor/manager/decision maker invests in equity.

B) MaxiMin Criteria (Risk Averter): If the decision maker is pessimistic or negative about the market, then s/he uses the maximin criterion of decision making. Under this criterion, the alternative is selected that gives the maximum out of the minimum return. In this example, the maximum out of the minimum is 5, which is given by Bond. So, the pessimistic decision maker invests in a bond.

C) MiniMax Criteria or Regret Criterion (Risk Neutral): If the decision maker is neutral, then s/he uses the minimax or regret criterion, where the decision maker minimizes the regret. So, the decision maker selects the alternatives that give the minimum from the maximum regret.

The regret table from the given example is:

Scheduling table

| Alternatives | Grow | Stable | Declines | Max |

| Bond | 25-15=10% | 20-10=10% | 0 | 10% |

| Equity | 0 | 20-20=0 | 20% | 20% |

| Mutual Fund | 5% | 5% | 15% | 15% |

Regret = Maximum pay off – realized pay off

Since the decision maker selects the option that gives the minimum regret from the maximum. In this example, 10% is the minimax regret given by the bond, and so the decision maker invests in the bond.

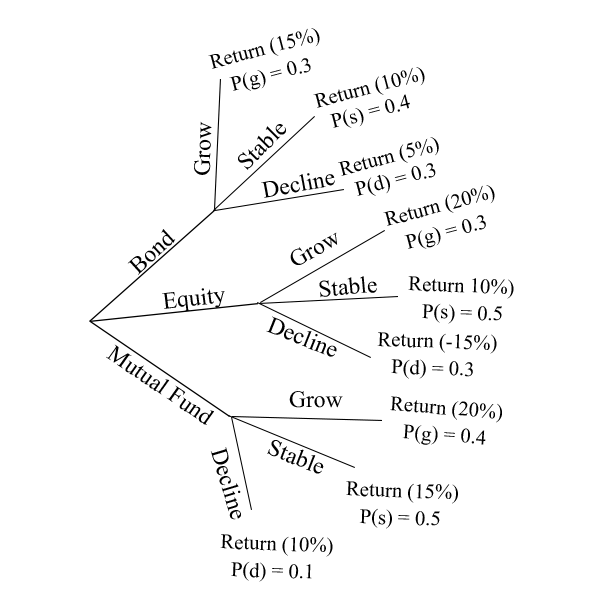

Decision Tree Analysis

It is also called expected value maximization. If the decision maker can assign the probability for the different states of nature, then s/he selects that alternative which maximizes the expected value.

In this approach, the different possible outcomes and the different states of nature with some probability are presented in a tree-like diagram. And calculate the expected value (profit, sales, market share), etc.

To explain this, consider the following example.

Here,

- The expected return from the bond = 0.3 x 15 + 0.4 x 10 + 0.3 x 5

- The expected return from the bond = 10%

- The expected return from the equity = 0.3 x 20 + 0.5 x 10 + 0.2 x (-15)

- The expected return from the equity = 8%

- The expected return from the mutual fund = 0.4 x 20 + 0.3 x 15 + 0.1 x 10

- The expected return from the mutual fund = 13.5%

Since the expected return from a mutual fund is higher, the decision maker invests in it.

Expected Utility Criterion (Utility is Subjective)

This is the more subjective criterion of decision-making, where the manager or decision-maker is assumed to maximize expected utility.

The decision maker can assign the utility for the different possible outcomes and the probability for the different states of nature. Then the decision maker selects that alternative which maximizes the expected utility.

To explain this, consider the following examples.

Scheduling table

| Alternatives | Grow | Prob. | Utility | Stable | Prob. | Utility | Decline | Prob. | Utility |

| Bond | 20% | 0.5 | 100 | 10% | 0.3 | 60 | 5% | 0.2 | 20 |

| Equity | 25% | 0.3 | 150 | 15% | 0.4 | 100 | -15% | 0.3 | 0 |

| Mutual Fund | 20% | 0.4 | 100 | 10% | 0.4 | 60 | -5% | 0.2 | 0 |

Now,

- Expected utility from bond = 0.5 x 100 + 0.3 x 60 + 0.2 x 20 = 72

- Expected utility from equity = 0.3 x 150 + 0.4 x 100 + 0.3 x 0 = 85

- Expected utility from mutual find = 0.4 x 100 + 0.4 x 60 + 0.2 x 0= 64

Since the expected utility from the equity is highest, s/he invests in equity

Other posts