Baumol developed the sales revenue maximisation model as an alternative to the profit-maximising model of traditional business. According to Baumol, in the modern corporate business, shareholders and management are two different parts of the organisation, where the shareholders have invested for profit, and the business is run by management. So, the objective of the modern firm is to maximise sales revenue by attaining a profit target to satisfy the shareholders and keep the job of the management secure.

i.e., Objective: Max TR = P.Q.

Subject to: πMin = π*

Where, P = price of product, Q = quantity of product, π* = minimum acceptable profit of shareholder

Baumol argues the following as the resource for maximising the sales objective of the firm.

- There is a positive correlation between the sales revenue and managerial benefits.

- The social image and market value of the firm and management are related to growing sales revenue.

- BFIs provide credit facilities based on the sales revenue.

- Sales revenue is considered an indicator of a business’s performance, meaning higher sales revenue implies improved performance, and it can be assessed daily/weekly or monthly, whereas profit-related information is available only quarterly or annually.

- Increasing sales revenue helps resolve the grievances of workers/staff and other stakeholders.

- The increased sales revenue can be used for strategic and competitive activities such as marketing, branding, innovation, and product diversification.

Therefore, the firm tries to maximise sales revenue, but it must provide a minimum acceptable profit to shareholders to keep management’s job secure. To explain this, Baumol assumes an imperfectly competitive market in the short run.

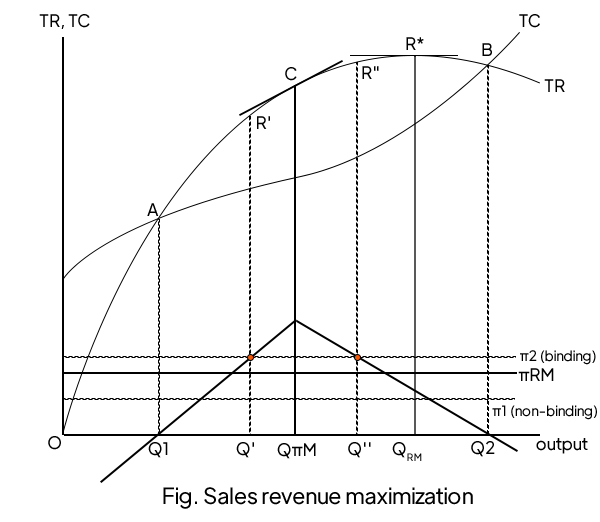

Here,

- TR and TC are the total revenue and total cost of the firm.

- If the firm produces less than Q1 or more than Q2, there is a loss.

- Sales revenue is maximum if the firm produces QRM quantity, and R* is the maximum revenue.

- If the firm produces QπM quantity, it maximises the profit.

- If there is no profit target given to the management by the shareholder, then the firm produces revenue-maximising output QRM provides πRM profit to the shareholder and enjoys the maximum sales revenue R*.

- But in this model, shareholders have given some profit target, and if such a target is π1 (less than πem) then this is not the binding constraint to the firm, and the firm produces revenue-maximising output QRM and provides πRM profit to the shareholder, which is higher than their target.

- But if the given profit target is π2 > πRM, then it is a binding constraint to the firm. It means the firm has to provide π2 profit to shareholders, which can be earned by producing Q1′ or Q” level of output. Since the objective is revenue maximisation, the firm produces Q” output because it gives higher revenue R” and R’.

- Therefore, in this sales revenue maximisation model, the firm tries to maximise the sales revenue under the given profit target as a constraint. This profit target is the minimum acceptable profit of the shareholder and is required to satisfy them, but such a target may be binding or non-binding to the revenue-maximising objective of the firm.

Other posts