Life Cycle Income Hypothesis (LCIH)

– Developed by Modigliani, Brumberg, and Ando (MBA)

This hypothesis was developed by the MBA during the 1950s, which argues that every rational individual tries to smooth out their consumption standard throughout their life, and so the consumption at any period depends on their lifetime income. The lifetime income is defined as the present value of expected income from both physical and human assets of the individual throughout their life.

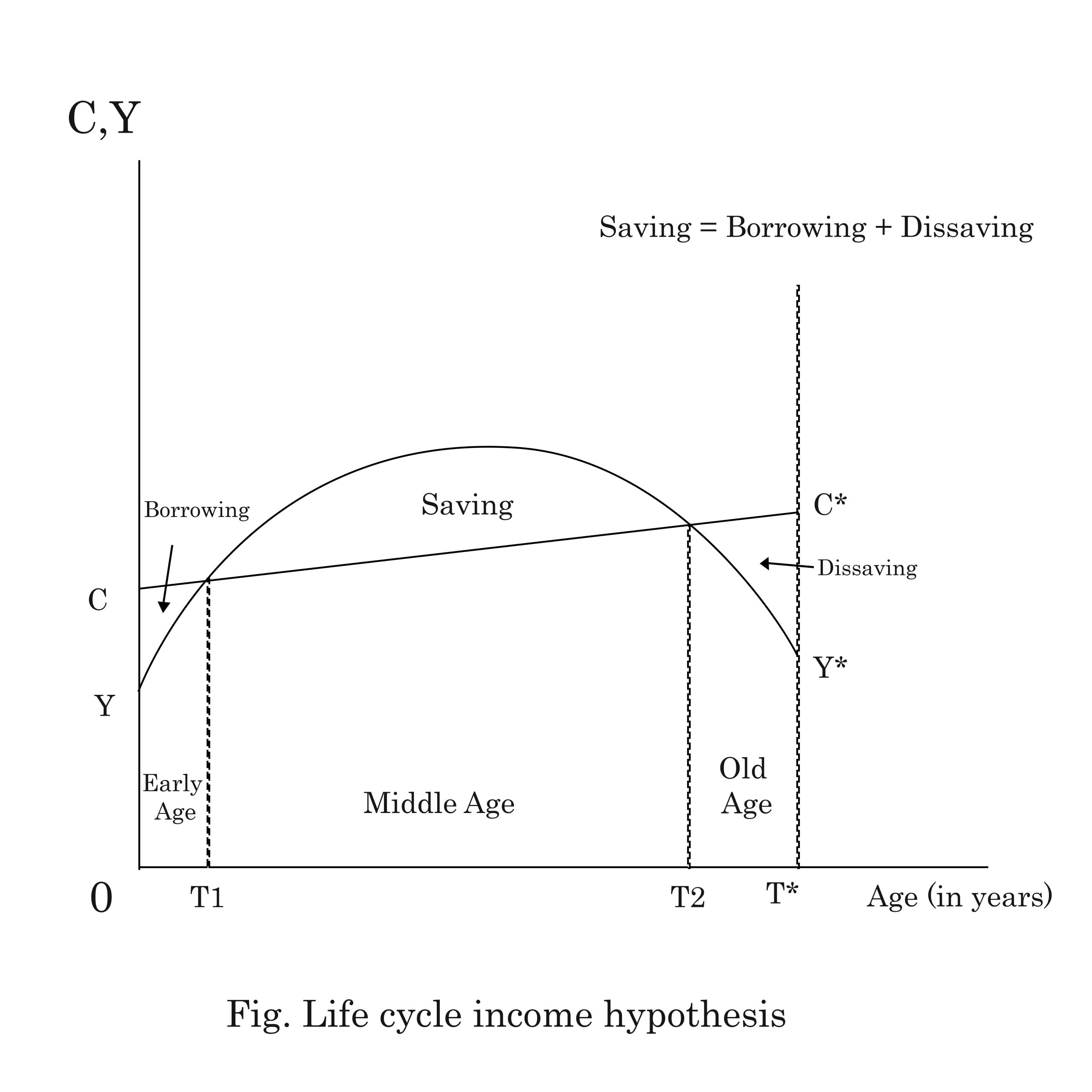

This hypothesis argues that the consumption of the individual is more or less stable or slightly increasing over age, but income shows a different pattern in the lifetime. At an early age, income is less than consumption, during which the individual is the borrower who borrows against future income. In the Middle Ages, income grew, reached a maximum, and then declined. During this period, income is more than consumption, which makes the individual save and save for the future or old age, and to repay earlier debt.

In old age, income is declining, and consumption is more than income, which is financed by dissaving from the savings of middle age.

Here,

- CC* is the lifetime consumption of the individual

- YY* is the lifetime income of the individual

- OT* is the lifespan of the individual

For an individual, OT1 is the early age at which the individual is born. In the middle age (T1 to T2), the individual is saver and in the old age (T2 to T*), the individual is dissaver.

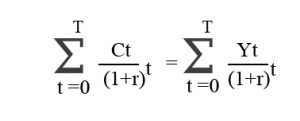

According to this hypothesis, the lifetime income and lifetime consumption are equal on average, where lifetime income and consumption are both in the present value of the firm.

i.e lifetime consumption = lifetime income

The lifetime income and consumption of the individual are equal, which means the individual has perfect information about the lifetime, which is the life expectancy from the macro perspective, and the individual neither receives inheritance from the ancestors nor leaves anything to the successors. (पुर्ख्यौली सम्पति पनि नलिने, सन्तानलाई पनि नछाड्ने).

It means whatever the individual earns in his/her life, they spend all of it.

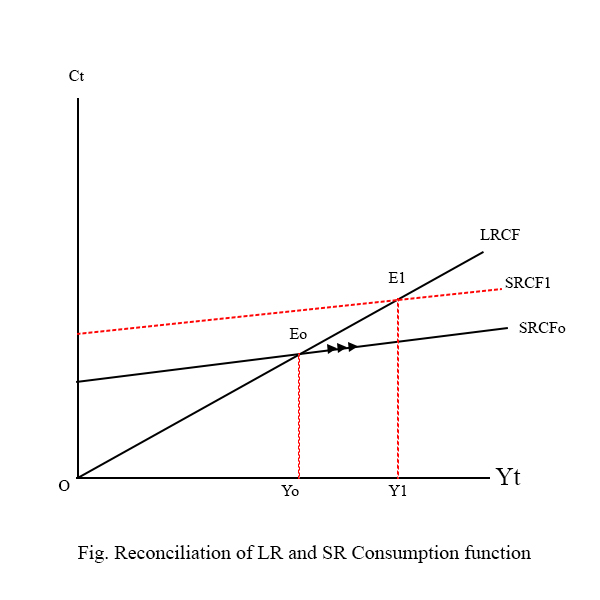

Though consumption depends on lifetime income in the short run, income and consumption are positive and non-proportional, but in the long run, they are positive and proportional. To explain this, this hypothesis argues that consumption at any period is a constant proportion of lifetime income, where lifetime income is defined as the present value of income from physical and human assets in their lifetime.

i.e. Ct = K PVt ————- (i)

- Where, Ct = consumption at t period

- PVt = present value of income from physical and human assets in the lifetime. (i.e., lifetime income)

- K = proportinality constant 0<k<1

Now, PVt = At + Ht ————— (ii)

- Where, At = present value of lifetime income from physical assets

- Ht = present value of lifetime income from human assets

According to Modigliani and others, if the financial market is efficient, then the current market value of the physical assets themselves is their lifetime income. So, it is easy to find At. However, it is not easy to find Ht, and they tested several hypotheses to find the expected labor income and found that labor expects their income based on current labor income, which is a certain times the current labor income.

- i.e. Ht = Lt + lte —————– (iii) Where,

- Lt = current Labor income, which is known

- lte = present value of expected Labor income from the remaining period

Now assume that ‘T’ is the remaining lifetime of the individual, where the income of the current period is known. So, the unknown period for income is (T–1) period. Let λ be the adjustment coefficient of expected labor income, then

- lte = (T – 1) α Lt

Substituting the value of lte in (iii)

- Ht = Lt + (T–1) α Lt

- or, Ht = [L + (1 + (T -1)α]

Again, we have

- Ct = K PVt

- or, Ct = K (At+ Ht)

- or, Ct = K [At + {1 + (T -1) α} Lt ]

- or, Ct = K At + K {1 + (T -1) α} Lt ] ——– (iv)

This equation (iv) is fundamental to the Life Cycle Income Hypothesis. According to this hypothesis, in the short run, income from physical assets is more or less stable, and the short-run consumption is affected mainly by the labor income, which makes SRCF positive non-proportional. But in the long run, the ratio of income from physical assets and total income (At/Yt) and the ratio of labor income and total income (Lt/Yt) remain constant, which makes the long-run consumption function positive and proportional.