Perfect Competition

It is the market structure where a large number of buyers and sellers, with homogeneous products, are present. The number of buyers and sellers is so large that there is a complete absence of rivalry between the buyers and the sellers.

Neither buyer nor seller can influence the market price, and the price is given to all of them, which is determined by the market or industry.

Basic Assumptions:

- A large number of buyers and sellers.

- Homogeneous product.

- Free entry and exit of the firm in the industry.

- No government intervention.

- Profit maximization objective of the firm.

- Perfect knowledge of the market.

- Perfect mobility of the factors of production.

Short Run Equilibrium: Price and Output Determination

In a perfectly competitive market, price is determined by the interaction between market or industry demand and supply, where the equilibrium price is that at which the demand and supply of the industry are equal.

i.e.DI = SI = P* (Equilibrium price)

Under this equilibrium price of the industry, each firm tries to maximize profit, where profit is the difference between total revenue and total cost.

i.e. Objective of firm: Maxπ = TR – TC

The profit is said to be maximum if the following two conditions are satisfied simultaneously.

- 1st order/necessary/primary condition: SMC = MR

- 2nd order/sufficient/secondary condition: Slope of SMC > Slope of MR, SMC must cut from below.

When the firm satisfies these two conditions, it is said to be in the short-run equilibrium, and in such an equilibrium, the firm may be in excess profit, normal profit, or in loss depending upon the cost condition and market demand of the firm.

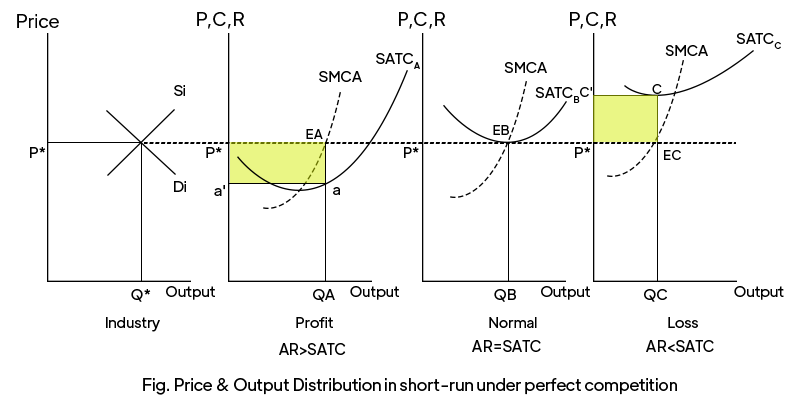

The perfectly competitive industry is in equilibrium at E*, where both demand and supply of the industry are equal. So, the industry equilibrium price is P*, and PQ* is the quantity. This equilibrium price, E*, is given to all the firms, and they try to maximize their profit under their own cost condition.

As in fig, the firm A is in equilibrium at Ea, where both conditions of profit maximization are satisfied. So, the firm A produces

OQA quantity at the given price P* and earns a profit equal to ☐ P*EAaa’.

Similarly, firm B and C are in equilibrium at EB and EC respectively, where firm B is in normal profit with OQB quantity at given price P*, and firm C is in loss of area ☐cc’P*Ec with OQc quantity and given price P*.

Therefore, in the short-run equilibrium, the perfectly competitive firm may be in excess profit, normal profit, or in loss, it all depends on the market price and efficiency or cost condition of the firm.

Long Run Equilibrium: Price and Output Determination

Since there is free entry and exit of the firm in the industry, all the firms are earning just normal profits in the perfectly competitive market in the long-run equilibrium.

If there is excess profit in the industry, then it attracts a new firm, which increases market supply. Under the given market demand, the increased market supply reduces the price and also the profit margin. The new entry will continue so long as there is excess profit in the industry and all the existing firms are in normal profit only.

Similarly, if there is a loss, none of the firms can continue their business with a loss in the long-run. So, the financially weaker firm quit the industry first. This reduces market supply and increases price under the given market demand. The increased price helps to reduce the loss of the existing firms, but those firms that are not able to manage their financial resources will quit the industry again once all the existing firms are in normal profit; no firms will be in the industry.

So, in the long-run equilibrium, all the existing firms are in normal profit, and there is neither entry nor exit of the firm in the industry.

i.e., for long-run equilibrium

DI = SI ⇒ P* (Equilibrium Price)

P* = MR = AR = LAC = LMC and slope of LMC > Slope of MR

Here,

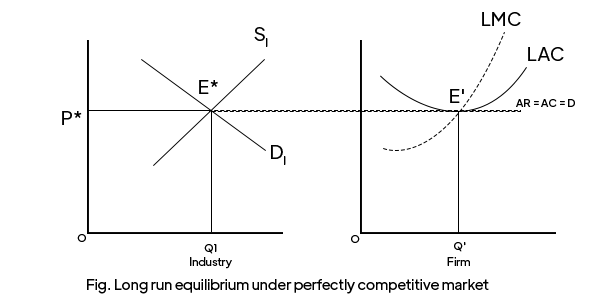

- The perfectly competitive industry is in equilibrium at E* with P* price and OQ* quantity.

- At P* price, the representative firm is in equilibrium at E’ with OQ’ quantity and is in normal profit.

- Therefore, while all the existing firms are in normal profit, there is neither entry nor exit of the firm, and the perfectly competitive market attains the long-run equilibrium.

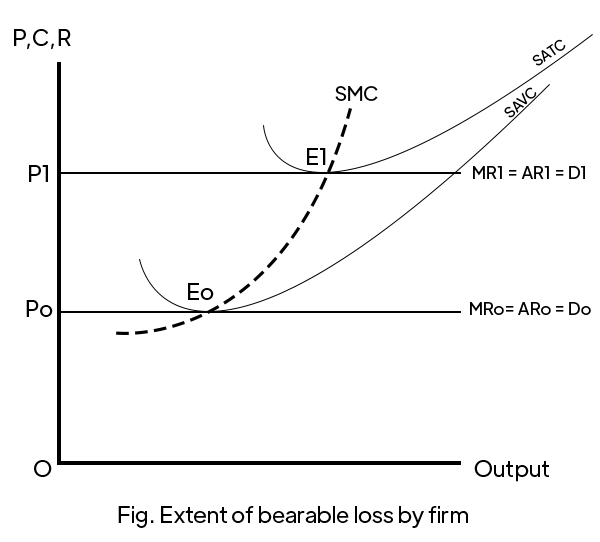

To what extent can a firm bear losses in the short run?

A firm may be in loss in the short run, but it does not mean that the firm can bear any infinite loss. So as long as the firm is able to cover the total variable cost, the firm continues its business, and if the firm is not able to cover even the variable or operating cost, a rational firm closes down.

Here,

- At P1 price, the firm is in normal profit, which means is price falls below P1, the firm is in a loss.

- But if the price is Po or above, the firm can cover its variable cost, and it bears other losses.

- If the price falls below P0, it can not cover the variable cost and closes down the business.

- So, the firm can bear a loss in the short run if the price is at the minimum or above the SAVC curve. i.e. P >=SAVC min

#Shutdown point

Price = SAVC

Other posts