It is the market structure where there is a large number of buyers and sellers and a differentiated but closed substitute product. Though the number os buyers and sellers is large, there is some degree of rivalness or competition among them. The firms compete with each other through selling activities such as marketing, branding, changing packaging, texture, colour, flavour, etc.

Basic Assumptions:

- A large number of buyers and sellers, but there is some rivalry or competition.

- Differentiated but close substitute products.

- Free entry and exit of the firm in the product group.

- No governmental intervention in the market.

- Profit maximisation objective.

Close Substitute = Technically and economically similar.

Product Group = Group of close substitutes

Price and Output Determination in the Short Run under a Monopolistic Market

Since the objective of a monopolistic firm is to maximise profit, the firm determines price and output to maximise profit given the demand and cost conditions. The firm’s profit is said to be maximised if the following two conditions are satisfied.

- First order condition: SMC = MR

- Second-order condition: Slope of SMC > Slope of MR, or SMC must cut MR from below

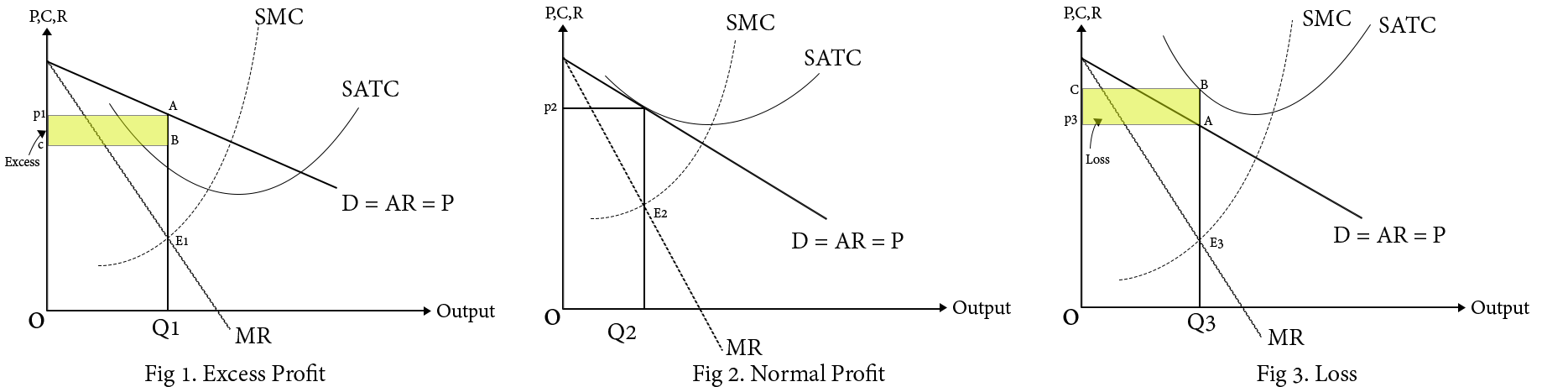

When these conditions are satisfied simultaneously, the firm is said to be in short-run equilibrium, and in such an equilibrium, it may be in excess profit, normal profit or in loss, which depends on the demand and cost structure of the firm.

- AR> SATC ⇒ Excess

- AR = SATC ⇒ Normal

- AR< SATC ⇒ Loss

Here,

- In fig 1, both conditions of equilibrium and profit maximisation are satisfied at E1, and so the monopolistic firm is in equilibrium at E1 with a p2 price and OQ1 quantity and earning an excess profit of ☐ABCp1.

- In fig 2 and fig 3, the firm is in equilibrium at E2 and E3, respectively. Where the firm in fig 2 is in normal profit with p2 price and OQ2 quantity, and in fig 3, the firm is in loss of ☐ABCp3 with p3 price and OQ3 quantity.

Long Run Equilibrium of Monopolistic Competition

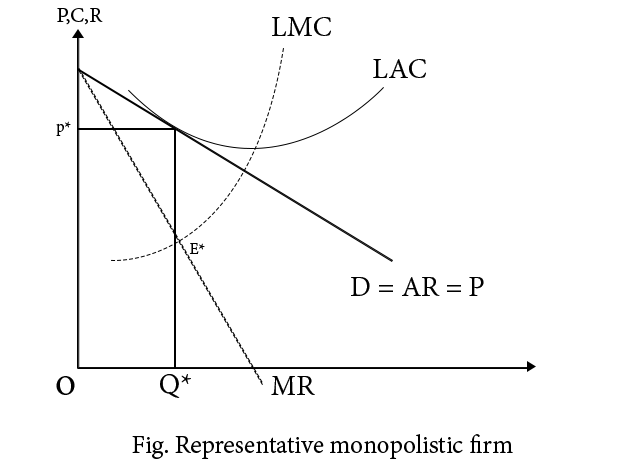

Since there is free entry and exit of firms in the product group, all firms in the group earn only normal profit in the long-run equilibrium. To explain this, we make a bold or heroic assumption,, such as.

- All the firms have identical costs and demands in the long run.

This assumption is required to explain the long-run equilibrium of the firm and the product group in the same graph.

As there is free entry and exit of the firms in the group, the new firms will enter if there is excess profit. The new entry of the firms increases the market supply, and under the given market demand, the price declines. This reduces the profit margin, and once all the existing firms are earning normal profit only, there is no new entry of firms.

Similarly, if there is a loss, the financially weaker firms quit the product group, which reduces the supply of the group. Under the given demand, the fall in supply increases the price, which helps to reduce the loss of the firms. When all the firms are earning normal profit only, there is no exit of the firms from the product group.

The representative monopolistic firm is in equilibrium at E*, where both conditions of profit maximisation are satisfied. So, P* and OQ* are the price and quantity at equilibrium where the firm is in normal profit.

Since all the existing firms are earning normal profit only, there is neither a new entry nor an exit of the firms from the product group. So, in the long-run equilibrium, the monopolistic competition market is stable with the existing number of firms and all of them are earning normal profit.

Other posts