This theory is also known as James Tobin’s speculative money demand theory.

- Keynes says Assets are (cash or bonds)

- Tobin says Assets are (cash and bonds)

This theory is an extension of the Keynesian speculative theory for money demand, where Keynes argued that the assets portfolio of an individual consists of either bonds or cash. But James Tobin reformulates this Keynesian theory, arguing that speculative demand for money is the issue of risk and return optimization.

According to Tobin, every rational individual diversifies the asset portfolio between cash and bonds. Holding cash is risk-free, but there is no return, and while holding a bond gives a return, it is risky.

In order to minimize the risk and maximize return, the rational individual diversifies the asset portfolio between cash and bonds. However, it depends on the individual’s preference for determining how much cash and how much bond to hold.

To explain this, assume that ‘r’ is the rate of return from the bond and ‘B’ is the no of bonds. Then, the total return from the bond (R) is given by

R = r. B

or, B = R/r ———— (i)

Similarly, assume that ‘j’ is the rate of risk, then the total risk (J) from B no of bonds is

J = j. B

or, B = J/i ——- (ii)

Now, from equations (i) and (ii), we have

R/r =J/j

or, R = r/j * J ———- (iii)

This equation (iii) shows the relationship between total risk and return. As r >0 and j>0. There is a positive relationship between R and J. This means the higher the risk higher the return.

This shows that the risk and return are associated with eachother where the individual has to bear some risk to have some return. It means it is the issue of risk and return optimization, and it depends on the individual preferences for taking risks.

It is assumed that the individual is the risk-return optimizer, where the utility function of the individual is given as:

U = f(R,J)

Where

- R = total return

- J = total risk

As the individual is rational, he/she tries to maximize the utility given by the return under the given risk.

i.e., Objective: Max U = f (R,J)

Subject to: R = r/j *J

This means the individual tries to maximize utility considering the given risk and return relationship represented by equation (iii). Since return is good and risk is bad, the utility function of the individual can be represented by the upward-sloping indifference curve. Then the individual is said to be in equilibrium by diversifying the asset portfolio between cash and bonds when the slope of the indifference curve and the risk-return line are equal.

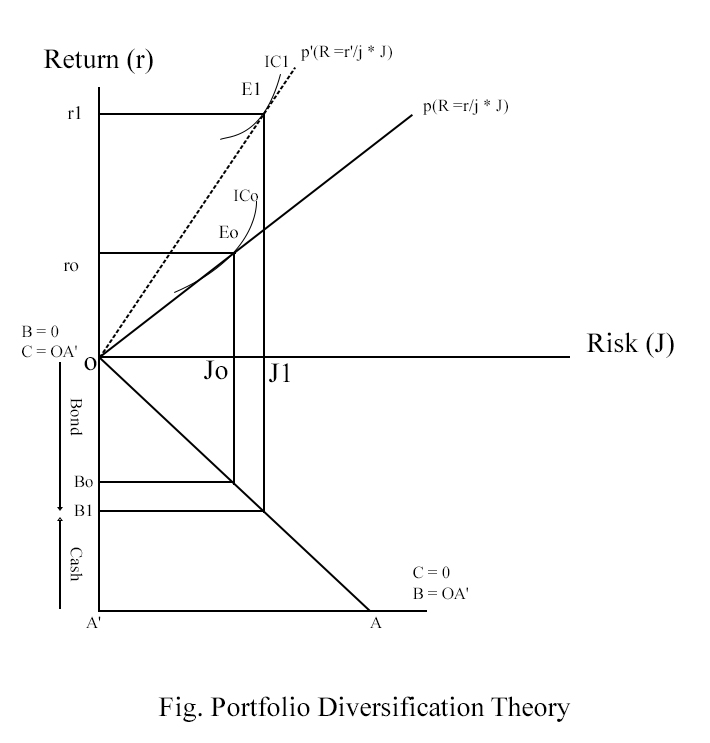

OA’ is the given asset of the individual, and OA is the portfolio diversification line. At ‘O’, there is no bond, only cash. i.e,. B =0, C = OA’ and ‘A’, there is no cash, only bond, i.e., C =0, B =OA’. So, O and A are the extreme points, which are the Keynesian Points.

Initially, the individual is in equilibrium at E0 with ro total return and Jo total risk, the individual holds OBo bonds and BoA’ cash such that OBo + BoA’ = OA’.

Now, other things remaining the same, the rate of return from the bond or interest increases from r to r’, then the individual attains a new equilibrium at E1 with a higher total return r1 and higher total risk J1.

For each higher return r1 and higher risk J1, the individual holds OB1 bond and B1A’ cash such that OB1 + B1A’ = OA’.

This shows that the rational individual diversifies the asset portfolio between cash and bonds to optimize the risk and return. If the rate of return from a bond or interest rate increases, the individual buys more bonds and holds less cash. This means the speculative demand for money is the inverse function of interest rate, which is similar to Keynesian speculative demand for money. The difference is only that the individual holds cash and bonds together under this portfolio diversification theory.

Relevancy of Money Demand Theories in the Context of the Digital Economy

The theories of money demand developed decades ago are still relevant in the context of a digital or cashless economy. The change is in the form of money but not in its uses or purpose. During the period when these theories were developed, it used to be physical cash, and now it is replaced by digital currency, but the function is almost the same.

The relevance of money demand theories in a digitalized economy can be shown as:

- The transaction motive of money demand still dominates. Even with digital wallets, cards, and QR payments, people need money for their transactions.

- The form of money has changed, but not the function. Though the currency is changed from physical to digital, the function of money remains the same as a medium of exchange, store of value, etc.

- The determinants of money demand are mostly the same despite the digital economy. Wealth, income, interest rate, expected return from other assets, and price level are still the major determinants of money demand.

- Due to lower transaction costs and rapidly growing digital infrastructure, the proportion of cash holdings is getting lower in recent years, which does not mean that people used to hold money by themselves, but nowadays, banks and financial institutions maintain the cash holdings on behalf of the general people.

- In the earlier days, there used to be limited choices for investment, but in the recent digitalized economy, there are a large number of alternatives due to rapidly growing financial technology, but still the decision of speculative demand for money depends on the expected rate of return of the other assets.