It is the market structure where there is a single seller and a large number of buyers, a unique product that does not have any close substitutes, and barriers to entry. Being a single supplier, the monopolist or firm has the market power to control the price and output, where the monopolist has two strategies: whether to charge a higher price by supplying a lower quantity or supply more at a lower price.

The following are the reasons for the occurrence of the monopoly market.

- The government policy of providing a license or patent right to a single firm.

- Limited size of the market that does not sustain more than one firm.

- Ownership of strategic raw material and technology by a single firm.

- The limit pricing policy adopted by the existing firm is to deter new entry.

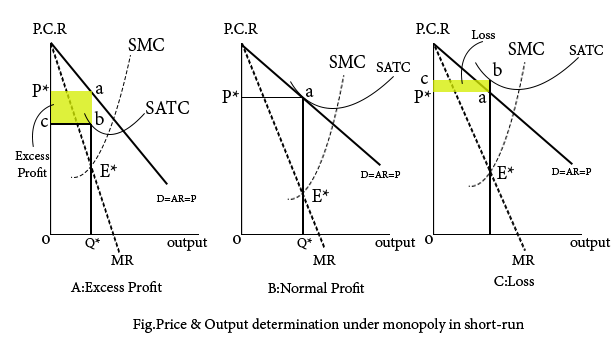

Price and Output Determination in the Short Run under a Monopoly Market

As the objective of the monopolist is to maximize profit, the price and output are determined at a point that satisfies the following two conditions of profit maximization.

- First order condition: SMC = MR

- Second order condition: Slope of SMC > Slope of MR, or SMC must cut MR from below

When these two conditions are satisfied simultaneously, the monopolist is said to be in short-run equilibrium, and in such an equilibrium, the monopolist may be in excess profit, normal profit, or loss.

It depends on the market demand and the cost condition of the monopolist.

Here,

Both conditions of profit maximization are satisfied at E* in all of these three cases, where the equilibrium price and quantity are P* and OQ*, respectively.

In fig A, the monopolist is in excess profit of ☐ abcP*, in fig B, the monopolist is in normal profit, and the monopolist is in loss of area ☐abcP* in Fig. C.

This shows that in the short-run equilibrium, the monopolist may be in excess profit, operating at normal profit, or in a loss. This depends on market demand or price and the monopolist’s cost conditions.

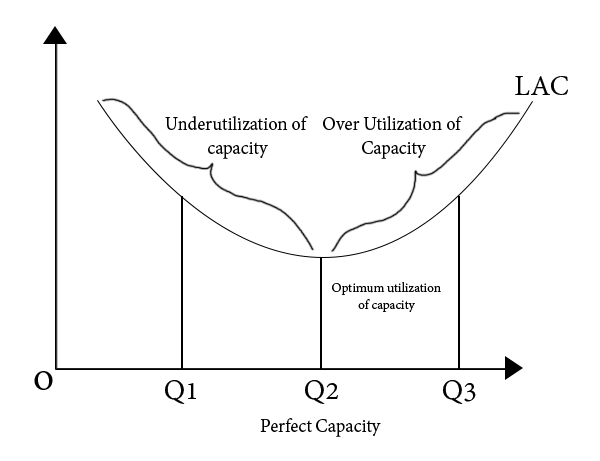

Price and Output Determination in the Long Run under a Monopoly Market

In the long run, the monopolist has enough time to adjust its products so as to meet the market demand. If market demand is small or limited, then the monopolist is in a long-run equilibrium at the falling part of the LAC curve or underutilization of the capacity. If the market demand is sufficient to operate at the minimum point of the LAC curve, then the monopolist is in a long-run equilibrium at the optimum utilization of the capacity, or at the minimum point of the LAC curve.

Similarly, if the market demand is great, then the monopolist is in long-run equilibrium at the rising part of the LAC curve or overutilization of the capacity. So, the long-run equilibrium of the monopolist depends on the market demand. Since there is a barrier to entry for new firms in the market, the monopolist generally earns excess profit but can not be in a loss in the long run equilibrium.

Here,

In fig 1, the monopolist is in long-run equilibrium at E1 with OQ1 quantity and Q1 price. Since this equilibrium quantity OQ1 is produced at the falling part of the LAC curve, the monopolist is underutilizing the capacity and earning excess profit of area ☐ABCp1.

In Fig. 2, the monopolist is in equilibrium at E2 with price p2 and quantity OQ2, at which LAC is minimum; this means the monopolist is at the optimum utilization of capacity in the long-run equilibrium and earning an excess profit of ☐AE2BP2.

Similarly, in fig 3, the monopolist is in long-run equilibrium at E3 with OQ3 quantity and P3 price. Since the LAC curve is rising at this level of output, the monopolist is operating at over-utilized capacity and earning an excess profit of ☐ABCP3.

Therefore, in the long-run equilibrium, the monopolist supplies to meet the market demand, where if the market demand is small or large, the monopolist supplies accordingly. Since there are barriers to entry of the new firms in the market, the monopolist generally earns excess profit in the long run. It may operate under the normal profit but can not be in loss in the long-run equilibrium.

Other posts