What is Cost Curve?

The cost curve is the graphical representation of the relationship between cost and output. So, cost curves are derived from the production function. The nature of production function affects the shape or nature of the cost curve.

Types of cost

- Explicit/direct/accounting cost

- Opportunity/implicit/indirect cost

- Economic cost

- Historical cost and replacement cost

- Separable cost and common cost

- Actual cost and opportunity cost

1. Explicit or Direct or Accounting Cost

It is the total payment/expenses made to the purchase and hire of factors of production used to produce the goods and services. It is the out-of-pocket expenses of the producer. These are the direct expenses of the producer to the supplier of the materials, rental cost paid to the landlord, interest paid to BFIs or money lender, wages and salaries given to the employees, etc.

Examples

- Wages paid to workers

- Rent paid for office or shop

- Electricity and water bills

- Raw materials cost

- Interest paid on a bank loan

2. Implicit or Opportunity or Indirect Cost

It is the cost related to the self-owned factors of production of the producers. If a producer uses their own capital, their own building, their own material, and works themselves in the business, there is no direct or explicit payment on such factor, which is the implicit or indirect cost. Such cost is calculated as the opportunity cost of the self-owned/produced factors of production.

Examples

- Owner’s own salary (not paid but sacrificed)

- Using your own building instead of renting it out

- Using your own capital in business instead of depositing it in a bank

- Owner working in their own business without taking a salary

3. Economic Cost

Economic cost is the sum of explicit and implicit costs. A rational producer is concerned with the economic cost in making a business decision, so, in economic analysis, we consider economic cost.

4. Historical cost and Replacement cost

Historical cost is the original amount of money paid to acquire an asset or resource at the time of purchase. It is recorded in the accounting books and does not change with market price fluctuations.

Replacement cost is the current amount required to purchase or replace an existing asset with a similar one at today’s market price. It reflects the present value rather than the past purchase price.

5. Separable cost and common cost

Separable cost is a cost that can be directly identified and assigned to a specific product, department, or segment. If that particular segment is discontinued, the cost will no longer exist.

Common cost is a cost that benefits more than one product, department, or segment and cannot be easily traced to a single unit. It continues even if one segment is stopped.

6. Actual cost and Opportunity cost

Actual cost is the real and measurable amount of money spent on producing goods or providing services. It includes expenses like wages, materials, and rent.

Opportunity cost is the value of the next best alternative that is given up when a decision is made. It represents the potential benefit sacrificed by choosing one option over another.

Cost Function

The functional relationship between the cost of production and its various determinants is called the cost function.

i.e. Cost = f(output, prices of factors, level of technology, gov. policy, allocation of firm, environment factor etc)

If we derive the relationship between the cost of production and the level of output, we get the cost curve. So, the cost curve depends on output, and cost curves are called derived curves. These are derived from the production function.

Traditional Theory of Cost Curve

The traditional theory argues that the per-unit cost curve is U-shaped in both the short run and the long run. Implying that, there is a unique combination between the per-unit cost and the corresponding level of output. Under the traditional theory, there are short-run and long-run cost curves given the short-run and long-run nature of production.

1) Short-run Cost Curve

i) Total Fixed Cost Curve (TFC): TFC is the total payment made to the fixed factor, and it is independent of output. So, the TFC curve has a positive intercept and is parallel to the output axis.

ii) Total Variable Cost Curve (TVC): TVCC is the total payment/ expenses on the variable factors. Initially, TVC increases at a decreasing rate and then increases at an increasing rate. So, the TVC curve has an inverse S shape and starts from the origin, implying that if there is no production, then there is no variable cost. Such an inverse S shape is due to the law of variable proportion operating in the short run.

iii) Short-run Total Cost Curve (STC): STC = TFC + TVC

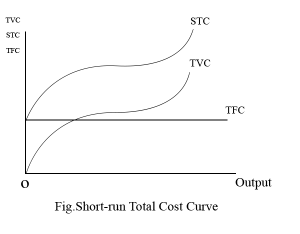

STC is the sum of the total fixed cost and the total variable cost, and so the shape of the STC curve depends on the shape of the TFC and TVC curves. As the TFC curve is parallel to the output axis and the TVC curve has an inverse S shape, the STC curve also has an inverse S shape, but it begins from the TFC curve, implying that even if there is no output at all, there is some short-run total cost.

Here, STC begins from TFC because at the origin, there is no output. i.e.

Output = 0, TVC = 0 then STC = TVC

STC has an inverse S shape due to the nature of the total variable cost curve. The gap between STC and TVC is constant, as the gap is TFC, which is fixed.

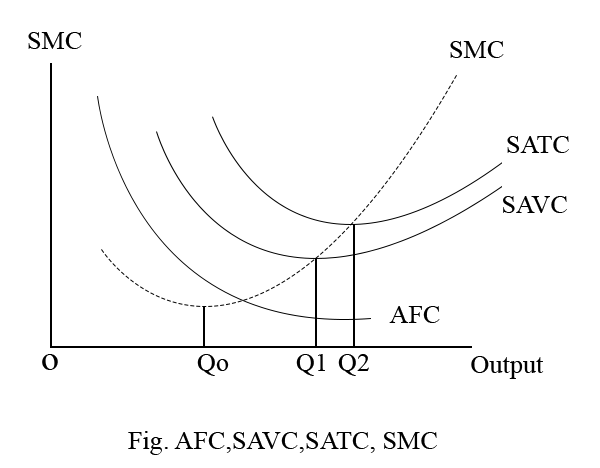

iv) Average Fixed Cost Curve (AFC): AFC is the per unit fixed cost in the short run. AFC = TFC/Q as the total fixed cost is constant, AFC continuously declines as the level of output increases, but it can not be zero. The shape of the AFC curve is a rectangular hyperbola.

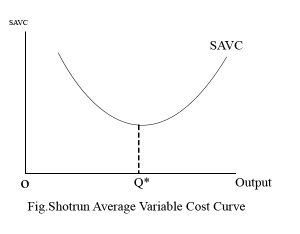

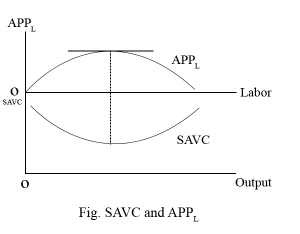

v) Short-run Average Variable Cost Curve (SAVC): SAVC is the per-unit variable cost in the short-run which initially declines, reaches a minimum, and then increases. So, the SAVC curve has U share, which is due to the law of variable proportion operating in the short run. SAVC = TVC/Q. If Q = 0 here, SAVC = TVC/0 ∴ SAVC = ∞

Here, SAVC initially declines up to the Q* level of output, and then it increases. i.e,. SAVC is minimum at Q*. This U shape of SAVC is due to the law of variable proportion, where initially the Average Physical Product (APP) of the variable factor is increasing, which reduces SAVC. When the APP of the variable factor is at maximum, SAVC is minimum, and when APP declines, SAVC increases.

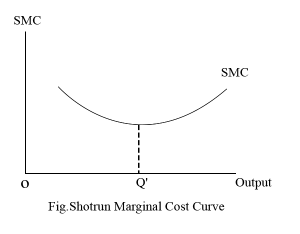

vi) Short-run Marginal Cost Curve (SMC): SMC is the additional cost due to an additional unit of output in the short run. SMC initially declines, reaches a minimum, and increases. So, the SMC curve is U-shaped, and it is due to the law of variable proportion operating in the short run.

Here, SMC is minimum at Q’ level of output, where the output is less than Q’, SMC is falling, and SMC is increasing for output more than Q’.

Relationship Among AFC, SAVC, SATC, and SMC Curve

Here, the AFC curve is continuously declining, but not to zero, and so the gap between SATC and SAVC is declining, but they do not intersect. The minimum point of the SMC curve is earlier than the minimum point of SAVC and SATC, and the SMC curve cuts both of them from their minimum points from below.

Similarly, the minimum point of SAVC comes earlier than the minimum point of SATC because, between Q1 and Q2, the falling rate of AFC is higher than the rising rate of SAVC. So, SATC declines continuously. But after the Q2 level of output, the rising rate of SAVC is higher than the falling rate of AFC, which increases SATC.

2) Long-run Cost Curve

i) Long-run Average Curve (LAC)

- It is a guideline curve

- It is a planning curve

- Tangential curve (SATC ko tangent)

- Envelope curve (It covers all the possible SATC curves)

Long-run Average Curve (LAC) represents the least possible per unit cost for the corresponding level of output in the long-run. Since it shows the minimum possible per unit cost, it helps to guide the firm to expand the business in the long-run. So, it is also called a planning curve. LAC curve is derived as a tangential curve of all possible SATC curves, which represent the possible alternative production units/plants.

As the LAC curve covers the entire SATC curve, it is also called the enveloped curve.

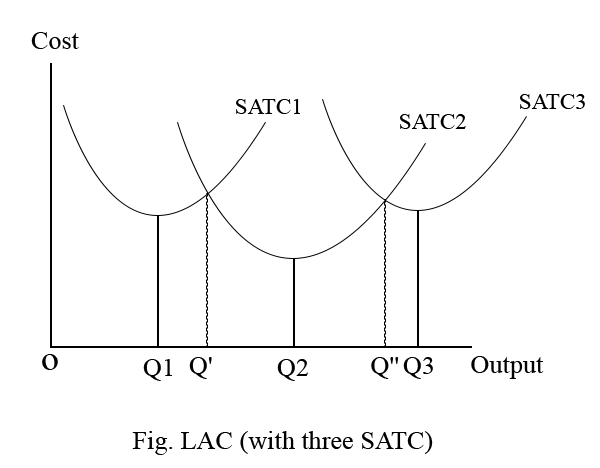

To derive the LAC curve, assume that there are three alternative plants available to the firm. Such as small, medium, and large plants. The corresponding SATC curves for small, medium, and large-sized plants are

SATC1, SATC2, and SATC3 respectively.

In the figure, if the firm plans to produce the Q1 level of output, then the firm installs the small-sized plant because none of the other plants can produce the Q1 level of output at a lower per unit cost than the small plant (SATC1).

Similarly, for Q2 and Q3 levels of output, the firm installs medium-sized and large-sized plants, respectively.

However, if the firm plans to produce Q’ level of output, then there is confusion about installing a small or medium plant because both plants can produce Q’ level of output at the same per unit cost. In this situation, the firm has to make a critical decision on whether to install a small or medium plant. If the firm expects the demand to increase further from Q’, then they install a medium-sized plant; otherwise, they install a small-sized plant.

Similarly, for Q” level of output, the firm installs a large-sized plant if it expects the market demand to increase from Q” in the near future; the firm installs a medium-sized plant.

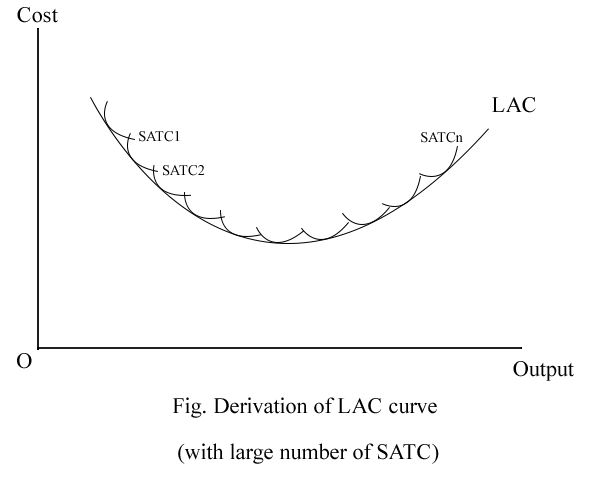

If we remove the consumption of only three alternative plants, and being realistic, there are an infinite number of alternatives available in the long run, with their own corresponding SATC curve. Then, if we draw a tenganbtial curve to all possible SATC curves, we get a smooth U-Shaped curve known as the LAC Curve, as shown in the diagram below:

Here,

- LAC is derived as a tangential curve to all possible SATC curves. Since there are such a large number of alternative plants, the LAC curve is smooth or continuous.

- LAC curve initially declines, reaches a minimum, and then increases, making it a U-Shaped curve.

- This U-Shape of LAC is due to the law of returns to scale operating in the long run, where the increasing returns to scale initially reduce LAC, and after a certain higher level of output, there are decreasing returns to scale, which increase LAC.

IRS (Increasing returns to scale) = Economies of scale. i.e., benefits from the large-scale production in the firm that reduces the per-unit production cost.

e.g., Large purchase of raw materials or large volume of borrowing/debt at a lower interest rate.

DRS (Decreasing returns to scale) = Diseconomies of scale. i.e., operating a low-occupancy flight, which results in a higher per-unit cost due to the large size of the firm.

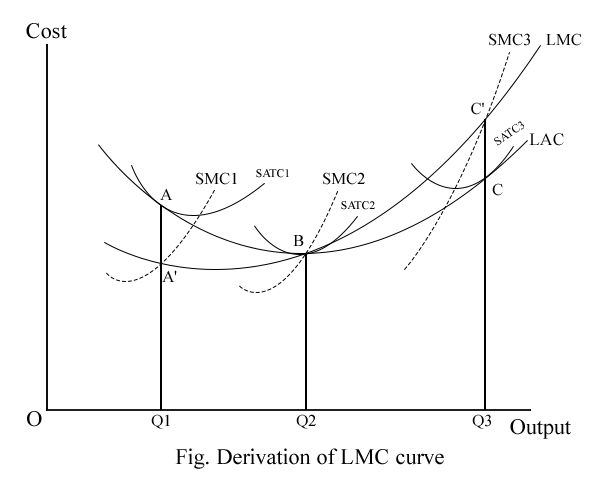

ii) Long-run Marginal Curve (LMC)

LMC is the change in total cost due to a change in a unit of output in the long-run. The LMC curve shows all the total costs changing in the long-run. The LMC curve is derived by joining the point of intersection between the SMC curve and a perpendicular line drawn from the tangential point of the LAC and SATC curve to the output axis.

To derive the LMC curve, consider 3 alternative plants with their respective SATC and SMC curve as:

Here,

AQ1, BQ2, and CQ3 are perpendicular lines drawn from the tangential points between SATC1 and LAC(A), SATC2 and LAC (B), and SATC3 and LAC (C). The points A’, B, and C’ are the points of intersection between such a perpendicular line and the corresponding SMC curve. When we join these points of intersection A’, B, and C’, we get the LMC curve. The LMC curve has a U-shape due to the laws of returns to scale operating in the long run, and the LMC curve cuts the LAC curve at its minimum from below.